SMM March 13:

This week, China’s domestic tungsten market exhibited high-level oscillations with intensified supply-demand competition. Multiple mines put products up for auction during the week, but transactions were bleak.As of March 13, tungsten prices remained largely stable, yet market sentiment became extremely divided.Upstream holders grew more risk-averse and increased shipments, while downstream buyers adopted a strong wait-and-see stance, restocking mostly under long-term contracts with very few spot transactions.The tungsten market abruptly shifted from a previous unilateral surge to low-volume,with a sharp contrast between holders’ reluctance to sell and downstream resistance to high prices.

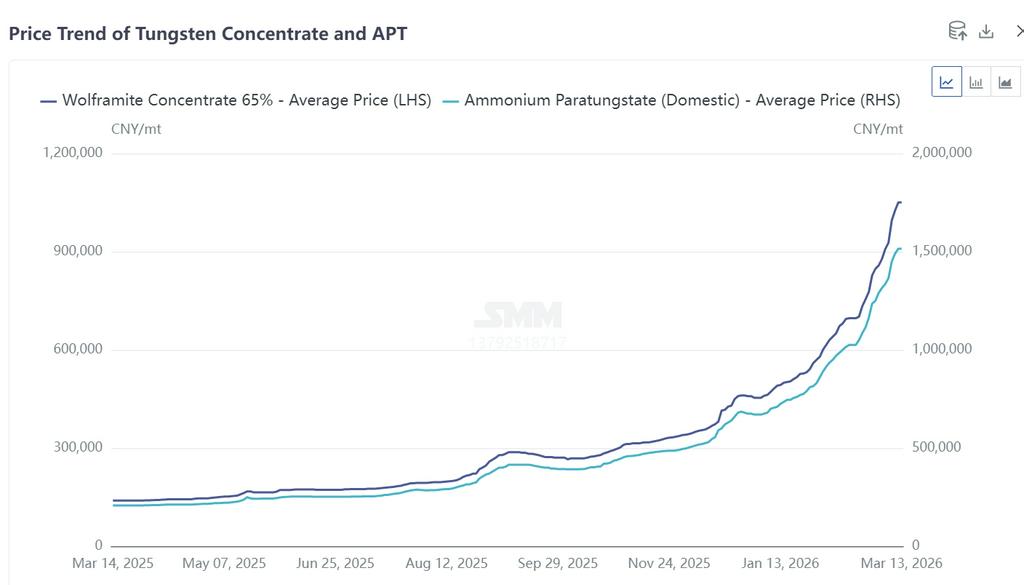

Tungsten Price Review This Week: High-Level Shock, Narrowing Gains

Since December last year, the tungsten market has entered a rapid rally. On March 10, tungsten ore prices jumped by 68,000 yuan per standard ton in a single day, hitting a record high.As of March 13, tungsten ore and APT prices have stalled and entered sideways consolidation.

- SMM 65% wolframite concentrate: Closed at 1.0505 million yuan/standard ton, flat from the previous day, up 131.6% year-to-date.

- SMM APT: Closed at 1.515 million yuan/ton, flat from the previous day, up 126.1% year-to-date.

Affected by pessimistic sentiment, some APT negotiated prices softened slightly within the day, with bargaining focus shifting below 1.5 million yuan/ton.Supported by strong costs, tungsten powder and tungsten carbide powder producers kept quotes steady.

- SMM medium-particle tungsten powder: Closed at 2,400 yuan/kg, flat from the previous day, up 121% year-to-date.

Why Did Tungsten Market Sentiment Reverse Abruptly This Week?

① Frequent Failed Mine Auctions

The market extended a sharp rally in the first half of the week, but sentiment turned cautious quickly on Thursday and Friday.The main trigger was that three mines in Hunan, Henan, and Guangdong successively auctioned low-grade tungsten concentrate from March 11 to 13.A total of 200 standard tons failed to sell, with very limited transactions.

High prices and cash-only payment terms raised funding pressure for buyers, reducing auction enthusiasm.Most domestic smelters cannot directly use low-grade ore, which requires traders to blend it with high-grade ore before delivery.Given the time lag between procurement and resale, traders feared price declines and subsequent losses, leading to failed auctions.

② Panic Selling in Tungsten Scrap Market, Leading a Mild Decline

Profit-taking pressure increased in the tungsten scrap market this week, causing prices to peak and fall.

- Tungsten scrap bars: mainstream non-tax-exclusive quote at 1,345 yuan/kg, up over 125% YTD and nearly 5 times vs. 2025 levels.

- Tungsten scrap drill bits: quoted at 1,320 yuan/kg, up 128% YTD, down 20 yuan/kg from the previous day.

Tungsten scrap mainly comes from mining tools, CNC cutters, tungsten wire, electronic components, and oil drilling bits.Qinghe in Hebei is China’s largest scrap cemented carbide distribution center, accounting for about half of national circulation.

After sharp price increases and stricter reverse-invoicing policies (individual annual quota capped at 5 million yuan), unqualified small workshops had to sell at lower prices to licensed enterprises, further weighing on scrap prices.

③ Divergence Between Tungsten Stocks and Spot Market; Stock Slump Spooked Sentiment

③ Divergence Between Tungsten Stocks and Spot Market; Stock Slump Spooked Sentiment

On March 13, the tungsten sector plunged collectively as profit takers sold off and capital fled for safety, dragging down spot market sentiment.

Outlook:

In 2026, the tungsten market has rallied sharply since the start of the year.Although supported by a supply deficit fundamentals, the market overheated after surging more than 100% in just two and a half months.Downstream sectors such as cemented carbide and end-use manufacturing paused buying due to cost pressure, switching to rigid small orders and sharply lowering trading activity, triggering a negative feedback loop.

Short term:Affected by excessive gains, downstream resistance to high prices, stock market cooling and profit-taking, the tungsten market will enter a pressure consolidation phase.

Medium to long term:The short-term sentiment shift does not mean a trend reversal, and the supply-demand structure remains tight.

- Supply: Tight mining quotas and strict environmental inspections persist. The first batch of mining quotas is due in April, which may temporarily ease tight supply but will not increase total volume.

- Demand: Solid support remains from PV tungsten wire substitution, military stockpiling, rising military demand amid conflicts, and growing aerospace consumption.

A widening global supply gap will underpin the long-term trend.The market will remain strong at high levels.Short-term focus will be on transaction activity, while medium- to long-term watch domestic mining policies and high-price transmission along the industrial chain.

![Titanium Market Structure Becomes Clearer: Upstream Consolidates at Weak Levels, Midstream and Downstream Strength Expected [SMM Titanium Weekly Review]](https://imgqn.smm.cn/usercenter/tjmLW20251217171722.jpeg)