SMM, February 23: During the Chinese New Year holiday (February 15–23), the overseas macro environment was complex, with Trump’s global tariff changes being the primary factor influencing market pricing over the break. According to reports, on February 21, US President Trump stated on social media that the "global import tariff" he announced the previous day would increase from 10% to 15%, effective immediately. At the same time, global geopolitical tensions remained highly uncertain. During the holiday, the US and Iran held a second round of indirect talks in Geneva, Switzerland, but significant differences persisted on core issues. Additionally, while the US Fed’s stance on interest rate cuts was relatively moderate, meeting minutes revealed that "a number" of officials were willing to consider rate hikes amid persistently high inflation—marking the first time in nearly two years that the Fed has discussed "rate hikes," reintroducing uncertainty to the US dollar interest rate path.

Amid these multiple factors, LME lead traded weakly and fluctuated rangebound during the holiday, moving within a range of $1,943.5–1,974/mt. As of 18:00 on February 23, it closed at $1,962.5/mt, down $9.5/mt from the pre-holiday closing price on February 13. In terms of inventory, LME lead inventory stood at 286,325 mt as of February 23, an increase of 53,675 mt compared to 232,650 mt before the holiday (February 13). Overseas lead ingot inventory buildup exceeded 50,000 mt during the holiday, which also contributed to keeping lead prices in the doldrums.

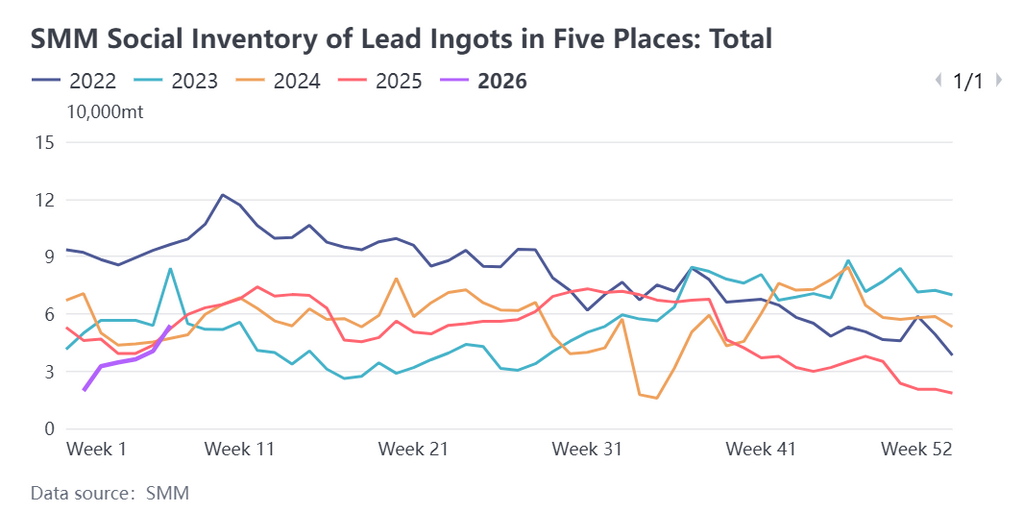

Today is the last day of the Chinese New Year holiday, and tomorrow, February 24 (the eighth day of the first lunar month), domestic exchanges such as the SHFE will reopen for trading, with SHFE lead returning to normal trading. For the post-Chinese New Year lead market outlook, our primary focus is on the lead ingot inventory buildup during the holiday period. It is understood that due to varying holiday schedules among upstream and downstream enterprises during the Chinese New Year, lead-acid battery enterprises—the main consumers of lead—were fully shut down for the holiday. In contrast, primary lead and secondary lead smelters had shorter holiday breaks than downstream enterprises, with medium to large primary lead enterprises largely operating normally. The absence of lead consumption during the holiday period is expected to lead to an increase in lead ingot inventory buildup expectations after the holiday. Notably, in the week before the holiday (February 12), the total social inventory of lead ingots across five regions monitored by SMM rose to 53,900 mt, the highest level in nearly five months.

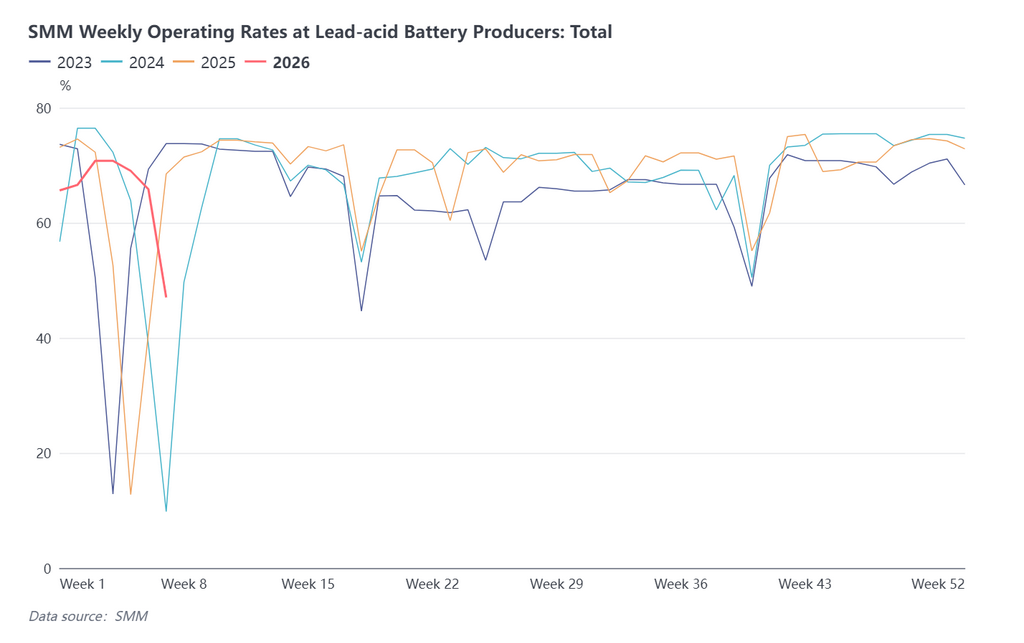

On the demand side, lead-acid battery enterprises are expected to resume production gradually from the first to the second week after the holiday. However, given that downstream enterprises generally maintain certain lead ingot inventories, procurement is expected to be limited in the first week after the holiday. Supply side, most secondary lead enterprises plan to resume production in the second week after the holiday, implying constrained market supply in the first week. Primary lead smelters, operating relatively normally, will be the main contributors to the lead ingot inventory buildup during the Chinese New Year period. Additionally, February 24 marks both the first trading day for SHFE lead and the delivery day for the SHFE lead 2602 contract, which is expected to bring some lead ingot shipments to delivery warehouses, transforming invisible inventory at smelter plants into visible inventory. The expectation of lead ingot inventory buildup is likely to be a key factor keeping lead prices in the doldrums in the initial post-holiday period. Subsequently, as downstream lead enterprises resume operations and lead consumption recovers, lead prices may have the opportunity to rebound.

![SMM February 13 EV Battery Market Summary [SMM Evening News]](https://imgqn.smm.cn/usercenter/xVUpr20251217171722.jpg)

![Pre-Holiday Trading Atmosphere Sluggish, SHFE Lead Records Doji [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/PKFMX20251217171721.jpg)