In 2025, driven by supply contraction and multiple demand growth, the global sulfur market saw supply-demand mismatch throughout the year, with prices rising sharply to new highs in recent years. Entering 2026, sulfur’s byproduct nature will constrain supply; Russia’s supply recovery will be slow; the Middle East will centrally control prices; the resonance of rigid demand from spring plowing and new energy “scrambling for sulfur,” together with heightened shipping risks in the Strait of Hormuz, will drive the global sulfur market to continue in a tight balance, keep the price center at elevated levels, and further reshape the regional supply-demand pattern.

2025 Review: Widening Supply-Demand Gap, Sharp Price Increase

(I) Supply Side: Pronounced Rigid Contraction, Intensified Regional Supply Divergence

According to the SMM survey, current global sulphur capacity is about 85 million mt. The industry is operating close to full capacity, but incremental supply is limited. Full-year production is about 80+ million mt, with a YoY growth rate of only around 2%, further slowing from about 4% in 2024.

As the core of global sulphur supply (with total Middle East production accounting for over 30% of the global total), some resources are prioritised for local markets and emerging markets such as Indonesia (long-term contracts first + high-price diversion). Resources exported to traditional demand countries have been heavily diverted, exacerbating tightness in resource circulation. Meanwhile, Russia, as a core global sulphur producer, has shifted from a net exporter to a net importer due to the Russia-Ukraine war. Coupled with shipping disruptions, geopolitical disturbances, and capacity release falling short of expectations, globally circulating resources remain persistently tight, driving sulphur prices higher.

(II) Demand Side: Stable Traditional Rigid Demand +Growth in Emerging New Energy, with a Significant Increase in Total Volume

In 2025, global sulfur demand presented a dual-engine pattern of “traditional rigid demand providing a floor, and emerging demand surging”: agriculture remained the largest consumption mainstay, with phosphate fertiliser production at its core forming a solid base of demand; traditional chemical demand such as titanium dioxide and caprolactam grew steadily; the new energy track saw explosive growth, becoming the core engine boosting incremental sulfur consumption. Together, these three sectors drove total sulfur demand to keep rising, in stark contrast to the rigid contraction on the supply side caused by its oil-and-gas associated nature.

Compared with previous years, the most notable change in the global sulfur market in 2025 was the explosive growth in new energy demand, which had become the central driver of incremental demand. Sulfur consumption in the new energy sector was highly concentrated in two major tracks—LFP and mixed hydroxide precipitate (MHP)—and formed a clear global regional division of labor: LFP production was highly concentrated in China, while MHP was focused in Indonesia; the two production hubs jointly dominated sulfur demand for new energy.

Against the backdrop of an accelerating global green energy transition, China’s NEV and energy storage industries have continued to expand. Leveraging core strengths of high safety, long cycle life, and significant cost advantages, LFP has become the preferred cathode material for large-scale energy storage and NEVs, boosting the continued expansion of domestic capacity. According to the SMM database, global LFP production reached 3.77 million mt in 2025, of which China accounted for 3.75 million mt, representing more than 99%, corresponding to a boost in total sulfur demand of over 3 million mt.

Meanwhile, relying on world-class laterite nickel ore resource endowments, Indonesia has vigorously developed HPAL hydrometallurgy, converting low-grade nickel ore into high value-added battery-grade nickel raw materials (MHP). By extending the industry chain and enhancing product value-added, it has become deeply embedded in the global power battery supply chain. According to the SMM database, Indonesia’s MHP production reached 443,900 mt Ni in 2025, directly boosting sulfur consumption by over 5 million mt; and after planned capacity comes on stream in 2026, Indonesia’s share of global MHP capacity will further rise from 67% to 77%, becoming the most explosive source of incremental sulfur demand globally and a key variable reshaping global sulfur trade flows.

Outlook for 2026: The Supply-Demand Gap Further Widens, and Prices Hover at Highs

In 2026, the global sulfur market further maintained a tight balance, with supply growth failing to keep pace with demand growth and the supply-demand gap widening further, becoming the core factor supporting prices fluctuating at highs.

(I)Supply Side: Limited Growth, Constrained by Multiple Factors

As a by-product of oil and gas extraction and refining, sulfur’s supply capability is highly dependent on the level of activity in global crude oil and natural gas production, while also being directly affected by geopolitical conditions, the smoothness of international shipping, and changes in trade policies. Disruptions at any stage will significantly impact the stability of global sulfur supply, the pace of price movements, and the distribution of trade flows. In 2026, the global sulfur supply side will exhibit operating characteristics of “constrained growth and a diverging regional landscape.” According to the SMM survey, incremental global sulfur supply in 2026 was only about 2.6 million mt, including about 500,000 mt in China and about 2.1 million mt in the Middle East.

According to the International Energy Agency (IEA), under the long-term trend of the global energy transition, global refining capacity and crude oil throughput are expected to enter a peak plateau around 2035 and then gradually pull back, which will fundamentally constrain the long-term growth potential of sulphur supply. According to the SMM survey, global crude oil demand growth in 2025 only remained at around 1%, with relatively weak growth momentum. As the core producing region for high-sulphur crude oil globally, the Middle East saw OPEC+ confirm a temporary pause in production increases in Q1 2026, further suppressing upstream supply elasticity.

Meanwhile, Iran has long been subject to US sanctions, with crude oil production and exports continuously constrained. The most-traded refineries in Russia continued to come under impact, with both production stability and logistics channels significantly affected; sulphur output and export capacity were sharply constrained and are expected to be difficult to recover in H1 2026, further exacerbating the tight globalised sulphur supply landscape.

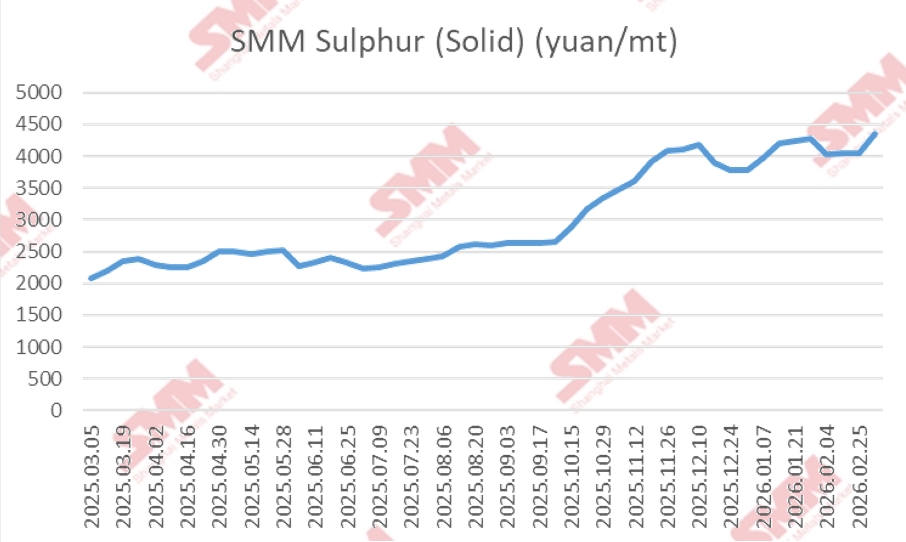

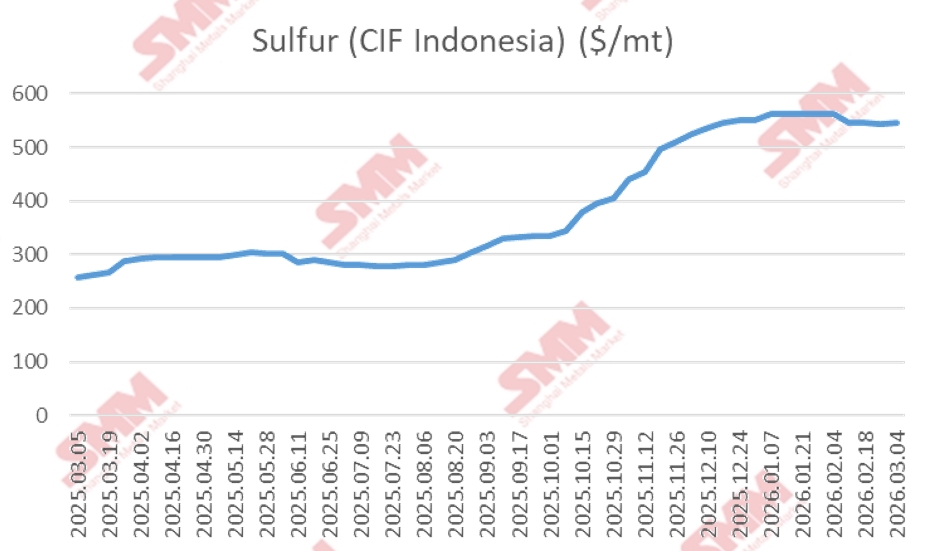

In early 2026, geopolitical conflicts in the Middle East intensified, and shipping risks in the Strait of Hormuz rose markedly; nearly 50% of global sulfur trade volumes passed through this corridor. Vessel detours, longer voyages, and a sharp rise in war-risk insurance premiums directly pushed up the landed cost of sulfur. In 2025, Middle East sulfur FOB prices climbed from about $170/mt at the beginning of the year to the latest level of about $520/mt, an increase of more than 200%. Meanwhile, continued turmoil in the Red Sea further extended shipping cycles and lifted overall import costs. Disrupted logistics and rising costs created dual pressure, reducing effective market circulation and slowing the pace of arrivals, becoming a key factor supporting sulfur prices fluctuate at highs.

The natural gas sector brought marginal improvement to supply: according to the latest quarterly report released today by the International Energy Agency (IEA), global natural gas demand in 2025 was about 1.3%. As a substantial increase in LNG supply eased market fundamentals and drove strong demand growth in Asia, global demand growth in 2026 will accelerate to about 2%. New projects in the US, Canada, and Qatar will come on stream in succession, and LNG supply is expected to increase by 7%, i.e., 40 billion m³. With natural gas consumption rising steadily, sulfur production as a by-product of natural gas desulfurization will increase accordingly, providing some supplementation to overall supply.

According to the SMM survey, global sulphur production growth slowed to 2.28% in 2025. In 2026, supply-side expansion will be limited, and supply growth will remain at a low level, with total annual supply expected to reach 82-83 million mt.

(II)Demand Side: New Energy-Driven, with Continuous Structural Optimization

Global sulphur demand in 2026 will sustain strong growth, with demand growth significantly outpacing supply growth. The key drivers are underpinned by rigid agricultural demand and a growth in incremental growth from new energy.

According to the SMM survey, global phosphate fertiliser consumption will grow steadily at an annual rate of about 1.6%. As the largest downstream demand segment for sulphur, it provides a solid foundation for the overall market; demand in the chemical sector will also expand steadily at an annual rate of about 4%–6%.

The most noteworthy incremental growth in 2026 will come from the concentrated ramp-up across the global new energy industry chain. According to the SMM database, newly built and commissioned LFP capacity in China in 2026 will exceed 2.5 million mt; together with the release of existing capacity, the industry’s effective capacity is expected to surpass 9 million mt, driving a sharp increase in demand for high-purity sulphuric acid and sulphur. Meanwhile, Indonesia’s nickel hydrometallurgy projects are accelerating, adding about 400,000 mt Ni of new MHP capacity. Based on its sulphur intensity of as high as 11.7 mt, this will generate incremental sulphur demand on the order of 1 million mt, creating a global “competition for sulphur” alongside global phosphate fertiliser, traditional chemicals, and new energy materials, further exacerbating tight global sulphur supply.

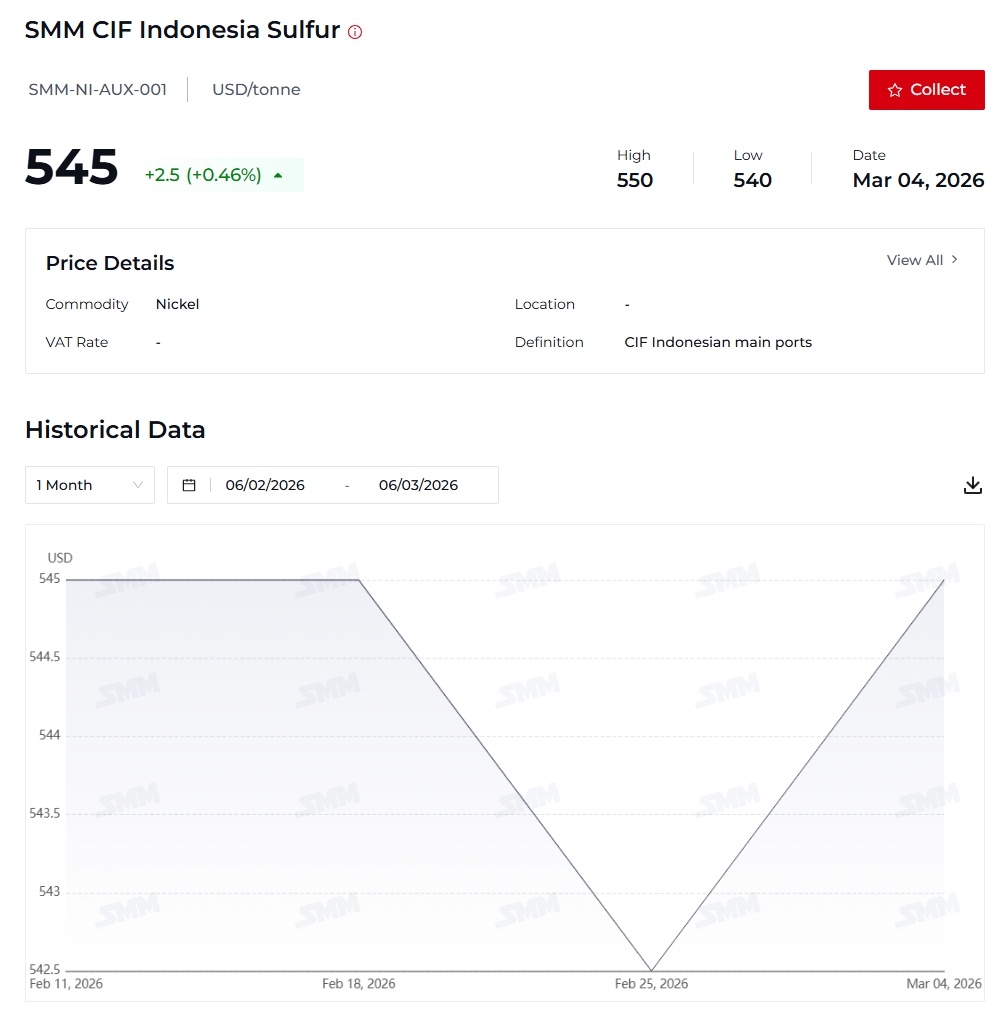

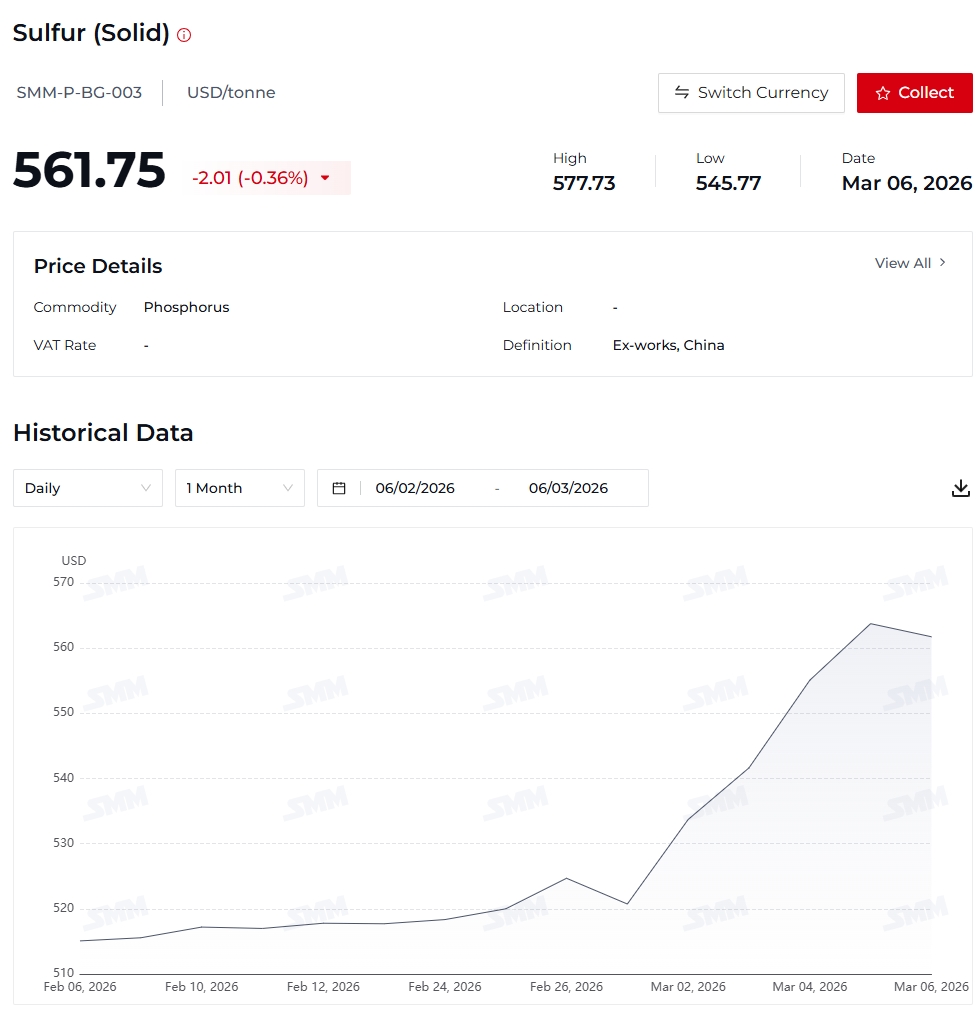

SMM has launched SMM CIF Indonesia Sulfur and Sulfur (Solid) price assessments for market reference.

SMM CIF Indonesia Sulfur Definition:CIF Indonesian main ports; Quality: Sulfur 99.5% min, Particle; Price Origin: Indonesia.

Sulfur (Solid) price Definition: Ex-works, China; Quality: Sulfur(S) 99.00% min,conforming to GB/T 2449-2006; Price Origin: China.

![[SMM Analysis] SS Weekly Review: Geopolitical Shocks and Cost Inflation Drive Prices as Market Faces Peak Season Test](https://imgqn.smm.cn/usercenter/fzwTi20251217171733.jpg)