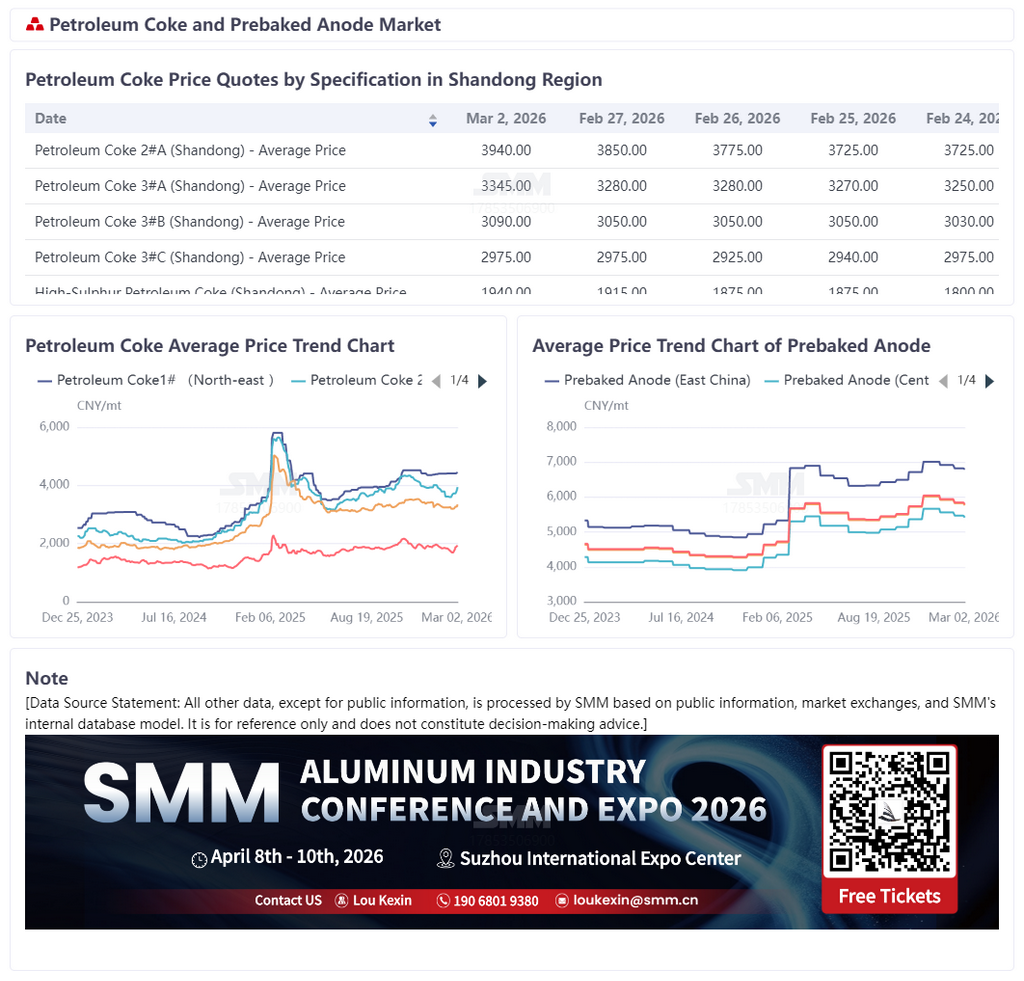

SMM March 2nd Report:

On February 28, 2026, the US and Israel launched a large-scale military strike on Iran, which promptly announced the closure of the Strait of Hormuz. The geopolitical situation in the Middle East escalated sharply and fell into sustained turmoil. As a critical "chokepoint" for global energy transportation, the Strait of Hormuz handles about 30% of global seaborne oil trade. Its blockade directly led to a severe physical disruption in the global energy supply chain, causing international oil prices to surge dramatically, with shipping costs and insurance fees skyrocketing, significantly increasing uncertainty in the energy market. As a key raw material for prebaked anodes used in aluminum production, petcoke is expected to enter a state of supply tightens, cost surges, and quality disturbances under the influence of the geopolitical situation. This change will directly impact the stability of China's petcoke import system, while also substantially raising domestic prebaked anode production costs, creating a chain reaction in the downstream aluminum industry.

In terms of the overall distribution of import sources, in 2025, regions and countries with high petcoke import dependency in China showed a tiered characteristic. The first tier, centered around the US and Russia, saw the US accounting for 31%, making it the largest source of petcoke imports for China; Russia followed closely with 17%, together contributing nearly half of the total imports. The second tier was the Middle East, collectively accounting for 15%, serving as an important supplementary segment for China's petcoke imports. Other import sources were more dispersed, with Canada and Brazil each at 5%, and Argentina, Colombia, and Taiwan, China, each at 4%. This diversification of smaller sources enriched China's petcoke import supply system, but the influence of individual entities remained relatively limited.

Notably, as a key supplementary sector for China's petcoke imports, the highly concentrated internal supply structure of the Middle East became the core reason for the impact of the deteriorating geopolitical situation on China's import market. In detail, the supply landscape of the Middle East exhibited a "dominance by one, supplemented by a few" feature: Saudi Arabia, with a 64% share, held an absolute dominant position, being the core exporter of petcoke from the Middle East to China; Oman ranked second with 22%; Kuwait accounted for 12%, with other regions providing only minor supplements. In terms of imported product specifications, petcoke from the Middle East mainly consisted of medium- to high-sulfur varieties, with different source countries focusing on specific types: petcoke from Saudi Arabia primarily included high-sulfur sponge coke and high-sulfur shot coke, from Oman mainly shot coke, and from Kuwait mainly medium-sulfur sponge coke. These types of petcoke are primarily used for blending in the production of prebaked anodes, serving as a crucial raw material supplement for the domestic prebaked anode industry. The blockade of the Strait of Hormuz has a multi-dimensional impact on the petroleum coke market: On one hand, the blockade leads to a complete halt in the export of Middle Eastern petroleum coke, significantly reducing the international circulation of petroleum coke. The arrival cycle for petroleum coke imported by China from the Middle East is notably extended, directly exacerbating the tightness of domestic import supply. On the other hand, some refineries in the region are affected by military conflicts, limiting their production activities and further contracting the overall supply of petroleum coke, creating a dual squeeze on the supply side. Meanwhile, the surge in international oil prices drives up the production costs of petroleum coke from refinery delayed coking units, providing a solid bottom support for petroleum coke prices. Coupled with the sharp rise in international shipping freight and war risk insurance premiums, these factors collectively push petroleum coke prices into a more likely to rise than fall trajectory.

In summary, this geopolitical conflict in the Middle East is a significant external shock to the 2026 petroleum coke-prebaked anode-aluminum industry chain. The triple pressures of supply tightening, cost surges, and quality disruptions will continue to be passed down: Petroleum coke prices will keep rising, pushing up the production costs of prebaked anodes, which in turn will elevate the production costs of aluminum. If the blockade of the Strait of Hormuz persists, the entire industry chain will gradually enter a phase characterized by high costs, low inventory, and strong fluctuations. Ensuring supply chain security and controlling enterprise costs will become the core challenges facing the industry.