Introduction

The 2026 Jolt: A Rocky Start for Upstream Nickel

Just over a month into 2026, the Indonesian nickel industry is already navigating a storm of uncertainty. What began as a mid-December whisper from the Indonesian Nickel Miners Association (APNI) regarding potential quota cuts has evolved into a full-blown supply crunch.

In early January, the Minister of Energy and Mineral Resources (ESDM), Bahlil Lahadalia, signaled that the 2026 RKAB production quotas would be tightly matched to smelter demand, hovering around 250–260 million wmt. However, as of February 11th, ESDM Minister Tri Winarno adjusted that figure slightly to 260–270 million wmt. While the numbers moved up, the sentiment remains clear: 2026 is shaping up to be a difficult year for miners, and the downstream smelter pipeline is looking increasingly vulnerable.

I. Review

Rewind to 2025: A Tale of Underperformance

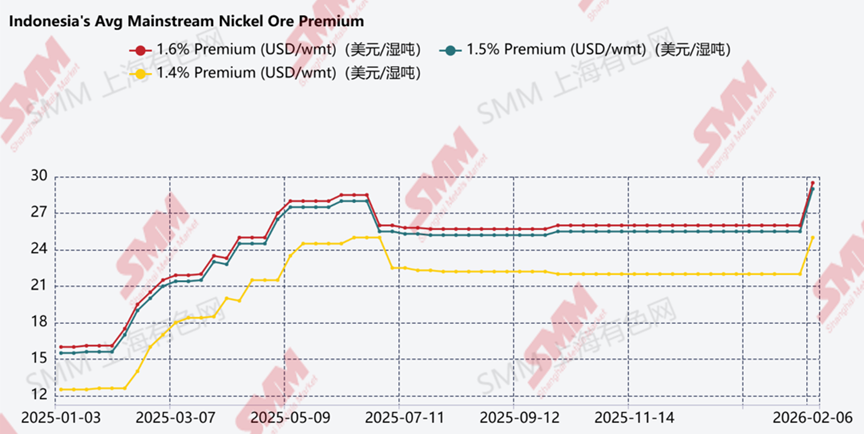

To understand the current market anxiety, we must look at the 2025 benchmarks. While the total approved quota for that year sat at approximately 330 million tonnes, actual production struggled to keep pace. Final output reached approximately 264 million tonnes, representing only about 80% realization of the approved volume.

This shortfall was primarily driven by heavy rainy seasons and chronic delays in both initial approvals and revisions. This scarcity pushed mainstream nickel ore premiums to reach between $25-$28, an all-time high for Indonesia in 2025. Until this February 2026, the premium spike is rather significant compared to last year.

II. 2026's Current Update

The Regulatory "Noose": Circular Letter 2.E/HK.03/DJB/2025

The ESDM has implemented a transition back to an annual RKAB cycle, which has created a massive administrative bottleneck. To prevent a total shutdown, the government released a "bridge" policy allowing mining companies to carry out exploitation activities up to a maximum of 25% of their previously approved capacity while awaiting final 2026 RKAB approval.

However, this safety net comes with strict compliance strings. To unlock the Mineral and Coal Online Monitoring System (MOMS) and facilitate sales, companies must meet three mandatory criteria:

- Submit a formal 2026 RKAB adjustment application.

- Settle all reclamation guarantees (Jamrek) for the 2025 production stage.

- Secure a valid Forest Area Utilization Permit (PPKH).

In reality, many mining operations are currently deadlocked due to administrative bottlenecks. Even with a prior 2026 approval, the MOMS system remains restricted for companies that haven't synchronized their latest compliance data, effectively halting sales and royalty payments, which results in low production and sale levels in the beginning of the year.

Substantial Quota Cuts: The "Big Two" Hit Hard

The most alarming signal for the market is the drastic reduction in quotas for the country's most influential mines. If the giants are being squeezed, the small and mid-scale miners face an even steeper uphill climb.

- Vale Indonesia's CEO, Bernardus Irmanto, confirmed a 30% cut compared to their initial application.

- Even more striking was the news from Eramet’s Press Release as of Tuesday, 11th February regarding Weda Bay Nickel (WBN, that they were approved for only 12 million tonnes—a staggering 71% drop from their 2025 annual quota of 32 million (and subsequent 36 million tonnes revision).

III. SMM's Analysis

The Supply-Demand Gap: Where is the Ore?

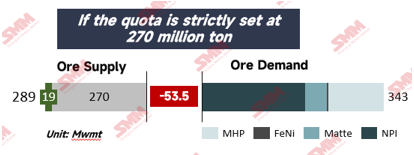

The math for 2026 simply does not add up. With the surge in HPAL projects in 2026, the demand for ore is skyrocketing due to higher unit consumption of ore from limonite. According to SMM, the total requirements will reach approximately 343 million tonnes this year. Against an ESDM quota ceiling of 270 million tonnes, the market is looking at a potential significant deficit.

While Indonesia is approaching the Philippines to bridge this gap, reliance on imports is risky. According to SMM, nickel ore imports from Philippines reached 15 million tonnes in 2025, and with a very optimistic view on 18-20 million tons in 2026 if quota revisions are not favorable and timely. However, risk still remain as Philippines' nickel mines are facing their own regulatory hurdles, including environmental compliance certificates and indigenous community consent, while also maintaining their supply lines to China.

IV. Conclusion

The Final Verdict: The Future "RKAB Revision Hero"

Is this the final word for 2026? Historical precedents indicate that the ESDM maintains a degree of flexibility for the approval processes in further months of revision. Minister Bahlil Lahadalia has publicly stated that RKAB quotas will be calibrated to align with actual industrial requirements, suggesting that the government intends to stabilize the supply chain to support consistent smelter production.

The primary attention now shifts to the Quota Revision which will be available for submission until the end of July. Most companies will inevitably seek revisions as their initial quotas are exhausted early. If the ESDM allows for even a 10–15% upward adjustment, it could provide the necessary breathing room for the MHP and NPI sectors. For now, the nickel market remains in a state of high tension, stakeholders remain focused on the government’s strategic direction: balancing the long-term objective of national mineral reserve preservation against the immediate operational demands of Indonesia's rapidly expanding downstream smelting capacity.

Currently, the nickel ore benchmark and premium prices have surged further, driven by persistent RKAB (Work Plan and Budget) uncertainties. While the commissioning of new MHP projects is expected to drive up unit consumption, these expansions are colliding with significant mining quota cuts. These converging factors, tightening supply and rising demand for intermediate products, are poised to propel nickel ore prices upward, echoing the volatility seen in early 2025.

To conclude, Happy Chinese Lunar New Year to everyone celebrating! Let’s hope to see further light in the nickel update soon—specifically, a timely RKAB approval that actually keeps pace with the smelters' appetite!

![[SMM Analysis] Ternary Cathode Market Sees Light Activity This Week Ahead Of Spring Festival](https://imgqn.smm.cn/usercenter/UruWE20251217171732.jpg)

![[SMM Analysis] Nickel Salt Prices Held Stable This Week as Trading Sentiment Weakened Approaching Chinese New Year](https://imgqn.smm.cn/usercenter/OjGlE20251217171734.jpg)