In early February, the rhenium market showed a diverging trend of cooling trading activity alongside rising prices. Affected by a mix of factors, supply-demand dynamics in the market have become increasingly competitive, market participants have grown more cautious, and the overall market has displayed distinct phased characteristics.

In terms of trading activity, market liquidity for rhenium weakened notably in early February compared with late January, mainly driven by sentiment spillover from the gold and silver markets. Recent price volatility in gold and silver has fostered a wait-and-see mood across the precious metals sector, which indirectly spread to scattered rare metals such as rhenium and slowed overall trading pace. Most market activity consisted of inquiries, with many investors remaining cautious; actual transactions were limited, supported only by small-volume rigid orders. Meanwhile, mild selling by retail investors emerged, reflecting uncertainty over the short-term outlook and further dampening trading sentiment.

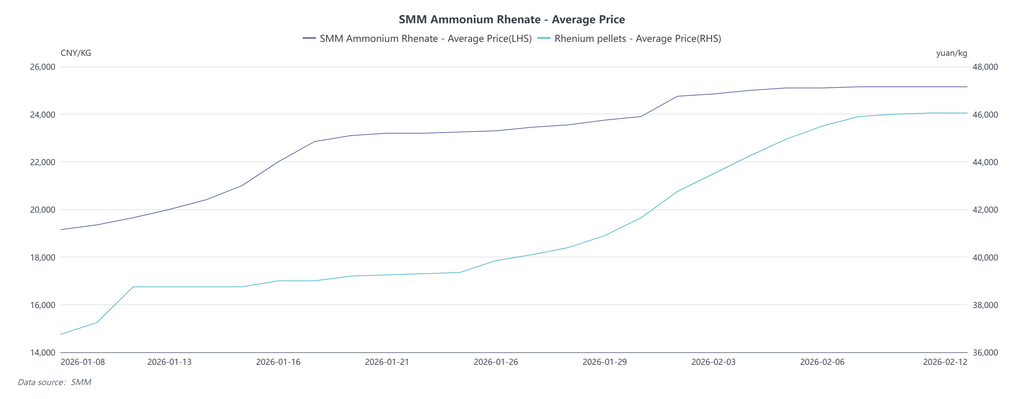

On the price front, despite weaker trading, rhenium prices remained firm and trended steadily higher, driven primarily by tight supply at the raw material upstream. Ammonium rhenate, the key feedstock for rhenium production, stayed in short supply with prices rising continuously, sharply pushing up raw material costs for downstream smelters. Supported by cost pass-through, end-product prices such as rhenium pellets also moved higher. However, as ammonium rhenate prices kept climbing, downstream smelters faced intense cost pressure. Some producers reported that price adjustments for finished products could not keep up with raw material inflation, squeezing profit margins, and a number of processors planned to raise the proportion of scrap recycling.

Looking ahead, the supply picture for ammonium rhenate may see marginal improvement. Attracted by expanding profit margins, many copper‑molybdenum smelters have begun considering recovering ammonium rhenate via smelting by‑processing, which would help ease tight supply to some extent. That said, rhenium is a scattered rare metal present at very low concentrations in copper‑molybdenum ores, and recovery involves technical barriers. Even with increased recovery efforts, output will remain limited, implying a persistent supply deficit in the ammonium rhenate market.

In terms of market expectations, the recent failed bidding for 3 tonnes of ammonium rhenate for Sinopec’s catalyst demand indirectly reflected producers’ optimistic outlook. Suppliers widely expect further upside for ammonium rhenate prices and were unwilling to sell in large quantities at current levels, resulting in the unsuccessful tender.

Overall, rhenium prices are expected to stay firm in the short term, supported by tight raw material supply and producer reluctance to sell. Over the longer term, rising recovery from copper‑molybdenum smelters may alleviate supply pressure, but a supply gap will persist. The rhenium market is likely to remain high and volatile, with industry profit distribution continuing to shift alongside changes in supply and demand.

![During the Pre-Holiday Period, the Magnesium Market Remained Stable, with Magnesium Ingot Prices Holding Steady in Major Production Areas. Overseas Inquiries Increased, but Trading Activity Was Sluggish [SMM Magnesium Weekly Review]](https://imgqn.smm.cn/usercenter/NPpAM20251217171723.jpeg)

![Gearing Up for 2026! Magnesium Market Ends January on a Stable Note, Nearly 300,000 mt of Demand Growth Boosts New Industry Prosperity [SMM Domestic Analysis]](https://imgqn.smm.cn/usercenter/FHiZE20251217171722.jpeg)

![[SMM Survey] Magnesium at the Crossroads: Utah Buys Polluted Magnesium Plant for $30M; Austria Advances New Alloy Tech](https://imgqn.smm.cn/usercenter/KXEYG20251217171725.jpg)