The beginning of 2026 did not bring the calm usually expected in the global stainless steel industry chain ahead of the traditional Lunar New Year offseason. Instead, under the double pincer attack of surging raw material costs and escalating trade protectionism, the market is undergoing a violent restructuring.

From Jakarta's suspension of sales offers to Brussels' tariff stick, and onto capacity expansion in Ha Tinh province, the main themes of the market in January can be summarized as: a return to "Cost-Based Pricing Power" and accelerated "Evasive Restructuring" of supply chains.

I. A Strong Counterattack from the Cost Side: Nickel Price Frenzy and Indonesia's "Pricing Power"

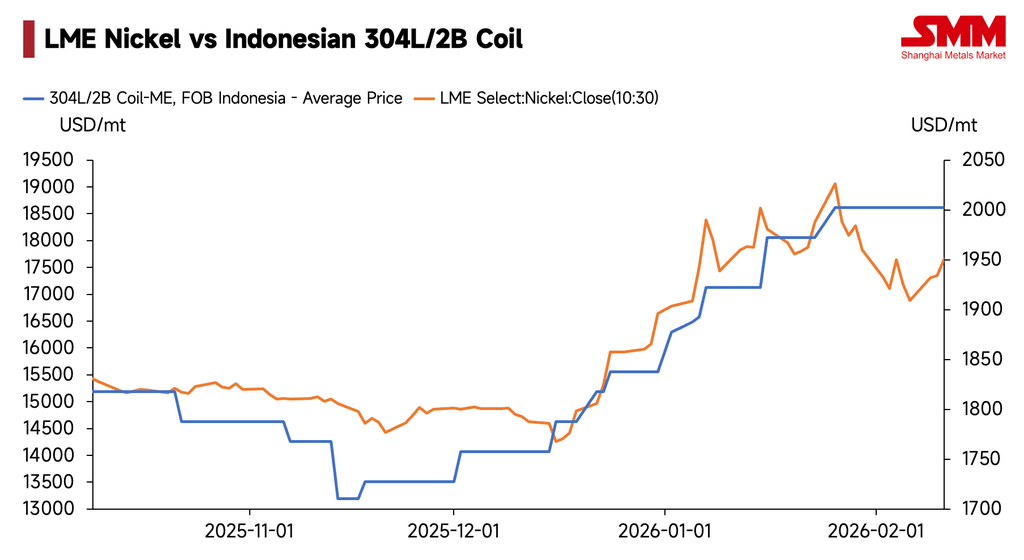

In January, the core driver of global stainless steel price trends originated upstream. With improved liquidity following the Federal Reserve's rate cuts, superimposed on fermenting rumors of production cuts in Indonesia, LME nickel prices broke through $19,160/ton in one fell swoop, hitting a new high.

The skyrocketing cost of raw materials directly activated the aggressive pricing strategies of Indonesian steel mills. During the month, mainstream Indonesian mills not only continuously raised export quotes (cumulative increase exceeding $110/ton) but also announced "stops on offers" (closing the order book) three times on January 6th, 15th, and 23rd. This rhythm of "price hike - suspend offers - hike again" not only reflects the mills' sensitivity to cost fluctuations but also demonstrates that, against the backdrop of tight nickel resources, the bargaining power of the seller's market is returning.

Transmitted through this channel, a "triple consecutive hike" for Taiwanese upstream steel mill list prices in February is now a foregone conclusion, with the market estimating an increase of $150-$200/ton. Meanwhile, although China's stainless steel exports hit a historical high of 485,000 tons in December 2025—overdrafting some overseas demand—global spot prices remain in a state where they are prone to rise and difficult to fall due to high cost support.

II. The "Besieged Fortress" of Trade Barriers: From European Battlements to the Southeast Asian Squeeze

If rising costs are the market's "internal fire," then the sharp tightening of global trade policies is the "external freeze." In January, the containment efforts by Europe, America, and certain emerging markets against Asian stainless steel reached an unprecedented intensity.

Europe: The Formation of "Double Pressure"

-

Tariff Storm: The EU plans to raise steel import tariffs to 50% and cut quotas, triggering collective protests from ten major European industry associations regarding "billions in surging costs."

-

CBAM Chaos: The Carbon Border Adjustment Mechanism (CBAM), which officially took effect on January 1, has faced industry backlash due to chaotic default value settings (e.g., semi-finished products from Taiwan, China having higher carbon emissions ratings than finished products), and even faces potential lawsuits. Foreign media have criticized the policy as being driven by "pure ideology," signaling that the hidden compliance costs for future exports to Europe will rise sharply.

The Americas and Southeast Asia: Escalating Containment

-

US Sanctions: The US Department of Commerce made a preliminary determination that the dumping margin for Vietnamese stainless steel pipes is as high as 90.80%. This constitutes a devastating blow to enterprises attempting to use Vietnam for transshipment.

-

Southeast Asia: Stricter customs inspections, fluctuations in tax collection scope and enforcement standards, as well as operational errors by enterprises regarding HS classification, rules of origin, and document consistency, can all trigger back taxes, port detention, return of goods, or even credit risks. The past route of relying on a "neighboring country pass-through" has seen its margin for error drop significantly in this environment. Enterprises are forced to reassess channel stability and compliance costs, shifting supply chain management from "seeking price advantages" to "controlling risk and delivery."

III. Supply Chain "Survival" and Restructuring: Capital Flows to Safe Havens

Capital is the most sensitive element when facing tariff barriers. The most shocking industry news in January was Yongjin Shares investing $380 million to build its first full-process stainless steel project in Vietnam.

The signal sent by this move is extremely strong: mere "product export" can no longer evade the stranglehold of rules of origin (such as US sanctions on simple processing in Vietnam). Only "full industrial chain export" that includes the smelting link can secure a legitimate "Non-China, Non-India" origin status. Yongjin’s construction of 2 million tons of hot rolling and smelting capacity in Vietnam is precisely intended to fill the upstream gap in Vietnam and build a secure supply chain moat.

At the same time, the transition to high-end products is accelerating. Whether it is Walsin Lihwa increasing capital in Yantai to deploy high-temperature alloys, or Outokumpu partnering with Metso to promote duplex stainless steel in battery metal equipment, it indicates that top-tier companies are attempting to offset the impact of trade barriers through technological barriers.

IV. Future Outlook and Strategic Recommendations

Looking ahead to February and the latter half of Q1, the market is more likely to maintain high-level volatility. The resilience of nickel prices and the market control exerted by Indonesian mills still provide cost support, meaning prices lack the basis for a deep fall. However, with the offseason for demand superimposed on uncertainties like strict Southeast Asian customs checks, fluctuating tax standards, and logistics delays, the transaction side is prone to a phase of "high prices but no market."

Strategy:

-

Downstream: Maintain necessary safety stocks and purchase in batches.

-

Export Enterprises: Prioritize solidifying channel compliance (Origin / Document Consistency / Carbon Data) to reduce risks of back taxes and port detentions.

The stainless steel market of 2026 is no longer just a game of supply and demand, but a contest of geopolitics and compliance costs. Amidst the storm, only those enterprises possessing global layout capabilities and technological moats can sail steadily and far.

Written by: Bruce Chew (bruce.chew@metal.com)

![[ NPI Daily Review ] Market Sluggish on Last Trading Day Before Holiday, High-Grade NPI Price Stable MoM](https://imgqn.smm.cn/usercenter/vcoVV20251217171732.jpeg)

![[SMM Nickel Sulphate Daily Review] February 13: Trading Sluggish Before the Holiday, Nickel Salt Prices Remain Stable](https://imgqn.smm.cn/usercenter/yaAtG20251217171733.jpg)

![[SMM Nickel Midday Review] Nickel prices experienced a significant correction on February 13, while the central bank conducted 1,000 billion yuan in outright reverse repo operations.](https://imgqn.smm.cn/usercenter/KFwsY20251217171734.jpg)