June 16, 2025

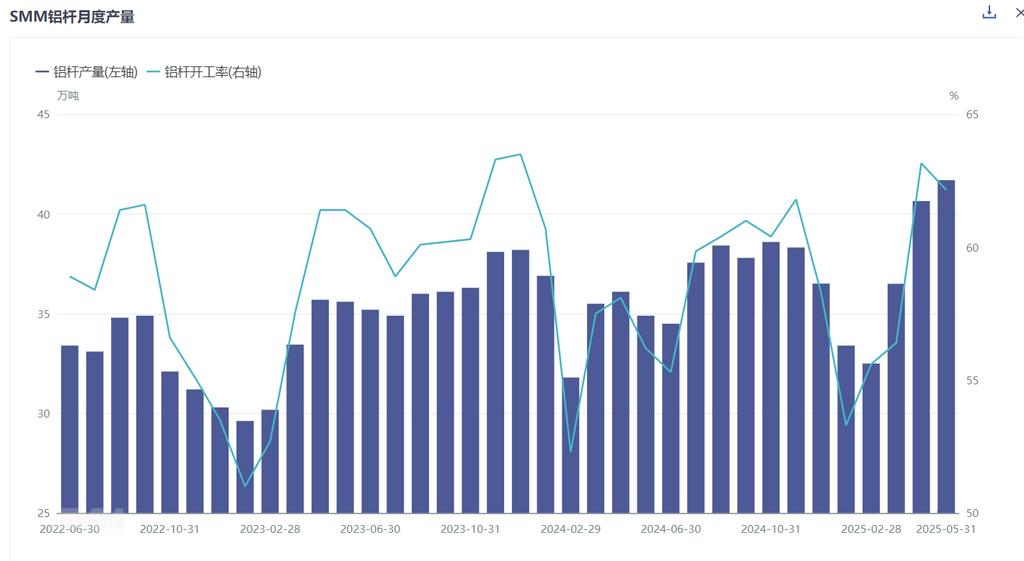

According to the latest monthly survey by SMM, China's aluminum rod production in May 2025 reached 417,000 mt, up 10,500 mt from April. After adjusting for the number of days in the month, the operating rate of aluminum rod plants in May stood at 62.15%, down 1.01% MoM but up 5.95% YoY. In early to mid-May, downstream purchases remained relatively stable due to weak aluminum prices and sufficient profit margins on orders on hand, coupled with the industry's concentrated shipment cycle, keeping supply-side operations at highs. However, by late May, futures aluminum prices held up well amid tight market circulation of aluminum ingots, while industry deliveries showed a clear weakening trend, leading to a rapid market downturn and a sharp pullback in processing fees.

Regionally, operating rates varied. As a hub for top-tier enterprises, Shandong saw its operating rate dip slightly to 86.4%, down 2.5% MoM. Inner Mongolia recorded an operating rate of 77.6%, down 3.1% MoM. Meanwhile, Henan, Guangxi, Guizhou, and Qinghai showed slight upward trends due to liquid aluminum alloying tasks and order conditions, while Ningxia and Shanxi experienced significant declines in plant operating rates due to partial capacity relocations and equipment maintenance.

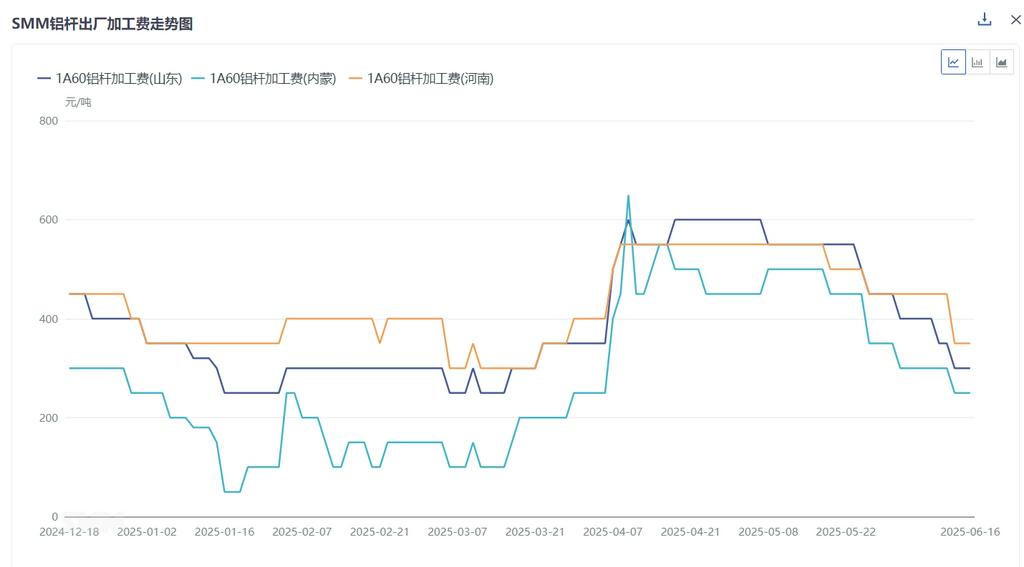

Market-wise, in May, downstream wire and cable factories began delivering orders for power transmission and transformation projects and backlog orders. Early to mid-month demand remained moderate, with aluminum rod plants maintaining smooth shipments and balanced production-sales. However, by late month, downstream delivery willingness weakened noticeably amid price rebounds, compounded by insufficient overhead line orders, leading to a clear shift in supply and demand dynamics. Circulating supplies gradually increased, pressuring aluminum rod processing fees downward. For high-conductivity aluminum rods, State Grid delivery orders remained the market's most-traded contract, with high-conductivity rods still a mainstream demand. However, as domestic high-conductivity rod technology evolved, industry barriers gradually dissolved, significantly reducing their premium capability. As of June 6, 2025, the average ex-works price of 61.5% IACS high-conductivity rods (Shandong) stood at 700 yuan/mt, while 62.5% IACS rods (Shandong) averaged 900 yuan/mt, down 200 yuan/mt MoM. For aluminum alloy rods, China's new PV installations from January to April 2025 reached 45.2GW, up 122% MoM, with the installation rush still stimulating alloy rod consumption. However, caution is warranted regarding potential post-531 policy period sustainability in PV installations.

SMM expects the aluminum rod market to enter an oversupply situation in June. Although the aluminum wire and cable industry's long-term rigid demand remains moderate, the concentrated delivery cycle has ended, with demand returning to normal levels. Meanwhile, plants have passed the pre-scheduling phase and entered an in-plant inventory accumulation cycle. SMM statistics show aluminum rod in-plant inventory accumulated for 3.7 days, up 2.4 days MoM. Therefore, against the backdrop of a slight rise in the center of aluminum prices in May, in-plant inventory increased while demand weakened, causing the center of processing fees to drop rapidly by 200 yuan/mt. It is expected that under the anticipation of continued weak demand, aluminum rod processing fees will remain weak and range-bound.