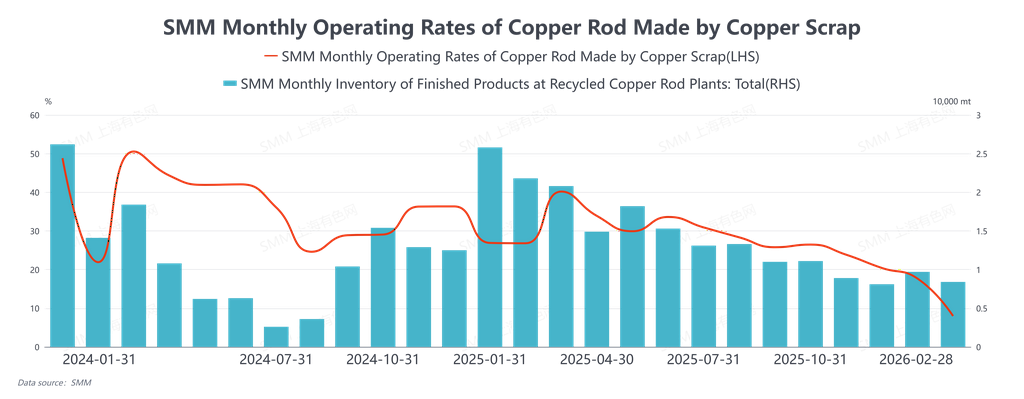

In February 2026, the operating rate of secondary copper rod was 7.98%, above expectations of 7.46%, down 9.7 percentage points MoM and down 23.72 percentage points YoY. In February 2026, China’s secondary copper rod market, jointly driven by the Chinese New Year holiday and policy uncertainty, went through a full cyclical evolution of “pre-holiday volatility and positioning, holiday trading stagnation, and delayed post-holiday resumption,” overall characterized by weak supply and demand and strong wait-and-see sentiment. In the final trading week before the Chinese New Year at the beginning of the month, the market saw wild swings driven by macro sentiment and financial arbitrage. Copper prices at one point neared the daily down limit; secondary copper rod enterprises generally suspended quotations, but actively purchased low-priced raw material to stockpile ahead of the holiday, with the operating rate holding at 14.82% that week. Notably, transactions were mainly driven by traders’ arbitrage based on the price difference between primary metal and scrap, highlighting the significant impact of financial factors on the spot market. Copper prices then rebounded sharply on policy-related news, and buyers and sellers engaged in cautious positioning amid rapid price surges and plunges. As the holiday approached, effective demand quickly fell to a standstill; the operating rate in the final pre-holiday week plunged to 7.35%, entering a typical “prices without a market” state, with price fluctuations completely detached from spot fundamentals.

After the Chinese New Year holiday ended, the market’s recovery progressed significantly more slowly than expectations, with policy wait-and-see sentiment becoming the core constraint. As of late February, the weekly operating rate of secondary copper rod was only 2.15%, plunging sharply YoY and remaining far below the same period in previous years. The pace of work resumption showed clear regional divergence: enterprises in Henan, Sichuan, Jiangsu, and other areas resumed production relatively actively, while those in Anhui, Jiangxi, Hubei, and other areas were comparatively sluggish. The root cause of the widespread delay in resuming production lay in policy uncertainty. Enterprises lacked clear expectations regarding issues such as the specific operational rules for “reverse invoicing” and whether local fiscal rewards and subsidies that were not delivered in 2025 would be disbursed, forcing them to adopt a cautious wait-and-see stance. Meanwhile, physical constraints in the production process (such as furnace drying for equipment) also extended the supply recovery cycle. The earliest batch of new finished products is expected to reach the market only in early March, resulting in a post-holiday supply gap. In contrast, waste-produced anode plate enterprises, constrained by long-term contract deliveries, saw a smoother production recovery, with a weekly operating rate reaching 7.45%. This further corroborated the current trend of structurally shifting demand for copper scrap toward the smelting end. Affected by the slow resumption of work among downstream processing enterprises and weak purchase willingness, transactions in the copper scrap market were sluggish, and inventories held by traders and main ports showed an accumulating trend.

Looking across February, market operations were successively dominated by pre-holiday financial fluctuations, the holiday’s natural pause, and post-holiday policy wait-and-see sentiment. Although the refined-to-scrap rod price spread provided some economic room for consumption, actual demand remained suppressed throughout. The core contradiction running through the month has deepened from a simple price game into a systemic stalemate jointly driven by unclear policy expectations and weak end-use orders. Looking ahead to March, as all links of the supply chain fully resume operations after the Lantern Festival, market supply will gradually rebound. However, the key for the industry to break out of the predicament still lies in whether the long-troubling fiscal and tax policies can become clear, and whether orders in end-use sectors such as real estate and the power grid can see a substantive recovery. After a period of quiet wait-and-see sentiment, the market will see its first concentrated test of the real supply-demand relationship in March.